Exploring the Semiconductor Industry: The AI-Driven Revival and What Lies Ahead

Will the Current Trend in TSM Continue?

Introduction

The semiconductor industry, a cornerstone of modern technology, is currently navigating a complex landscape. As we moved into 2023, the industry wrestled with worldwide economic and geopolitical challenges. Rising interest rates, high inflation, declining consumer confidence, and tech-led downturns in the stock market have led to a significant loss in market capitalization over the past two years. The combined market cap of the top 10 global chip companies has plummeted by 34%, from US$2.9 trillion in November 2021 to US$1.9 trillion in November 2022.

Interestingly, the semiconductor industry experienced a revival in November 2022, coinciding with the Artificial Intelligence (AI) boom triggered by the announcement of ChatGPT by OpenAI.

I may agree with Herb Greenberg the AI boom has the potential of becoming a bubble that may burst at one point in time, as he mentioned in his latest post: “But if we learned nothing else during the SPACs, the crypto, the meme stocks, and whatever else fueled the market's last run – you know, the one when stocks were the only place to put your money because rates were so low – it's that when this stuff reverses, it's always brutal.”

I do not know whether we are already in the mania phase. Still, this AI-driven revival has added a new dimension to the industry's growth story, emphasizing the increasing relevance of AI in shaping the future of semiconductors. The rise of Artificial Intelligence has become a major investment trend for the future. Of course, there will be ups and downs along the way.

A recent KPMG and the Global Semiconductor Alliance (GSA) survey reveals an optimistic outlook among semiconductor executives about the industry’s future growth. Key findings from the survey1 include:

81% of executives expect company revenues to increase in 2023.

67% identify talent risk as the top strategic priority for the next three years.

52% believe chip supply shortages will ease by mid-2023.

24% believe there is currently a semiconductor inventory excess, and the supply chain shortage is over.

46% plan to diversify their supply chain geographies in the next 12 months.

The top 10 biggest semiconductor companies by revenue include Taiwan Semiconductor Manufacturing Co. Ltd. (TSM), Intel Corp. (INTC), Qualcomm Inc. (QCOM), Broadcom Inc. (AVGO), Micron Technology Inc. (MU), NVIDIA Corp. (NVDA), Applied Materials, Inc. (AMAT), ASE Technology Holding Co. Ltd. (ASX), Texas Instruments Inc. (TXN), and Analog Devices Inc. (ADI). These companies are expected to profit significantly from the AI boom in the industry.

As part of my analysis, I have looked further into Taiwan Semiconductor Manufacturing Co. Ltd. (TSM), a prominent player in the industry.

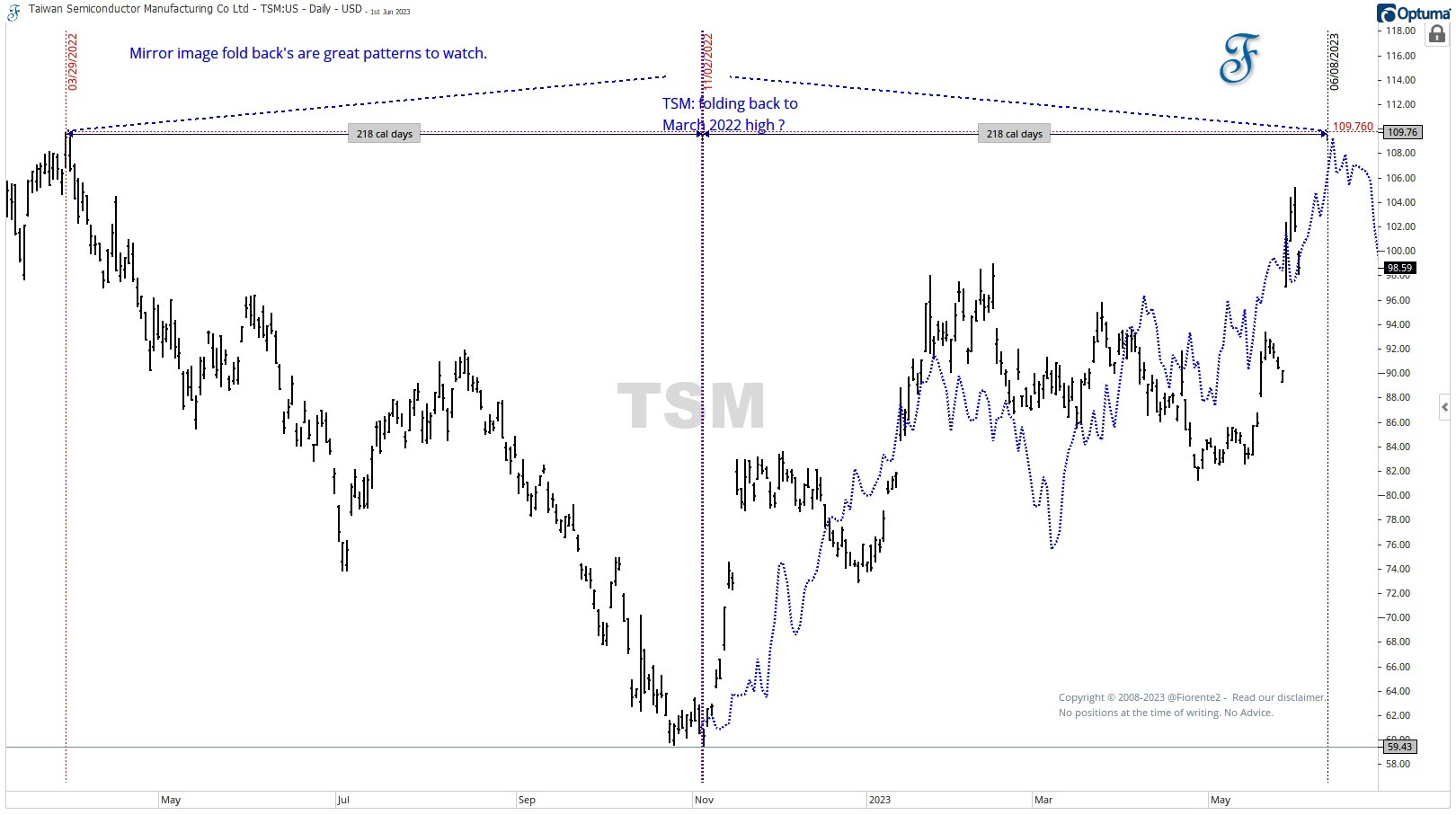

Recently, I noticed an interesting pattern in TSM’s chart that started with a low in November and seemed to be driving the stock back to its previous price levels, as shown in the above chart. Mirror image fold-back patterns are great to follow, but at some point, they will cease functioning, and a new trend may start.

What is possibly driving this fold-back? Will this trend continue? In the following analysis on TSM, you can read more about this pattern, the currently active cycles, and what to expect for the future of this stock in price and time.

This analysis is intended for general informational & educational purposes only. Hypothetical or simulated performance based on past cycles has many limitations. Cycles can contract, extend, and invert. Anomalies can occur. Hence, past performance is no guarantee for the future. No advice. Please take a look at our full disclaimer.